#1 Printing Money

Printing money, Is it okay? Everyone else is doing it why should I be concerned about the value of the dollar if the EU, GB, Japan, China, and other nations are printing money to fund the pandemic. The US has printed about $9 Trillion in 2020 which equates to about 22% of the total money in circulation

- People say the Fed is printing money when it adds credit to accounts of federal member banks or lowers the fed funds rate.

- The Fed does both of these actions to increase the money supply.

- The Bureau of Engraving and Printing, under the U.S. Department of Treasury, does the actual printing of cash for circulation.

I go back and forth with family and friends on this topic. What is all this printed money going to do to the market and the value of the dollar. Only time will tell.

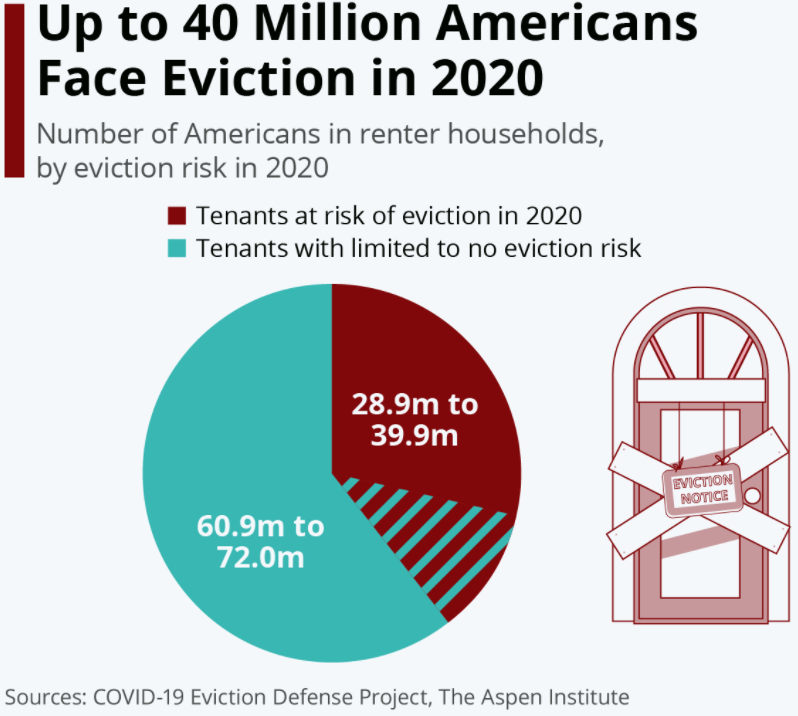

#2 Evictions & Unemployment

Evictions will begin and jobless claims are still increasing. By January 31, 2021 the ban on evictions will end and landlords will start to remove tenants who cannot pay their rent. People have been sitting around waiting for the government to solve this issue but need to realize it is going to take every person in the world to overcome this pandemic, unemployment, and economic turmoil.

In the week ending January 9, the advance figure for seasonally adjusted initial claims was 965,000, an increase of 181,000 from the previous week’s revised level. The previous week’s level was revised down by 3,000 from 787,000 to 784,000. The 4-week moving average was 834,250, an increase of 18,250 from the previous week’s revised average. The previous week’s average was revised down by 2,750 from 818,750 to 816,000.

Even with holds on evictions and people living off stimulus checks how much longer with the government keep supporting them. Yes, stimulus checks will be running until September and minimum wage has been increase to $15, but citizens cannot keep piggy backing off the government and stimulus forever. Yes it is working right now but the longer we do this the more damage will come down the road.

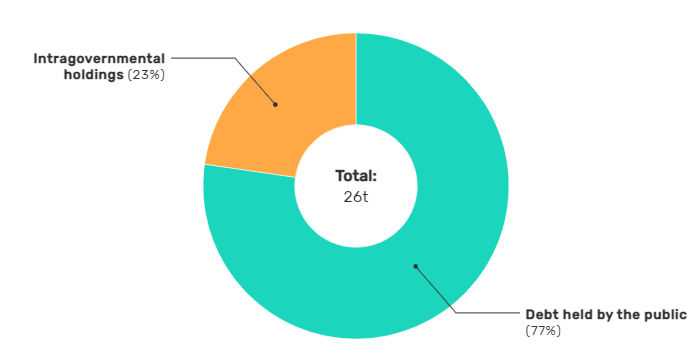

#3 US Debt

We have added $7 Trillion in debt and the total debt of the US is $27 Trillion. One question… who are we in debt to? Simply put, the public holds about 77% of the debt and the other 23% is by Intragovernmental Holdings or foreign countries. The public counts for $21 Trillion and consists of US Banks and Investors, Federal Reserve, State and Local Governments, mutual funds, pensions funds, insurance companies, and savings bonds.

As of July 2020…

Our foreign debt is about $6.81 Trillion in which Japan and China are responsible for $1.29T and $1.07T respectively.

In the end…

Many people believe that much of U.S. debt is owed to foreign countries like China and Japan. The truth is, most of it is owed to Social Security and pension funds. This means U.S. citizens, through their retirement money, own most of the national debt.

U.S. national debt is the sum of these two federal debt categories:

- Public debt (held by other countries, the Federal Reserve, mutual funds, and other entities and individuals)

- Intragovernmental holdings (held by Social Security, Military Retirement Fund, Medicare, and other retirement funds)

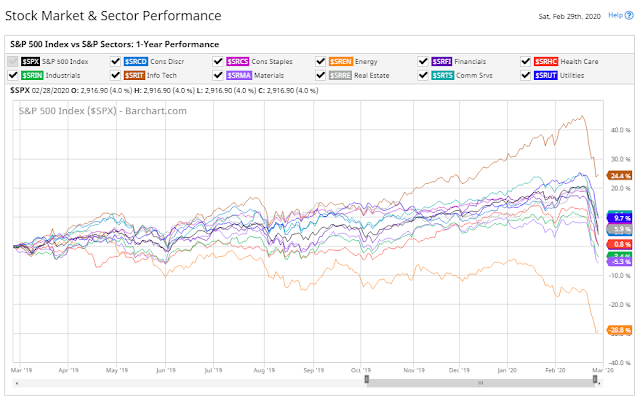

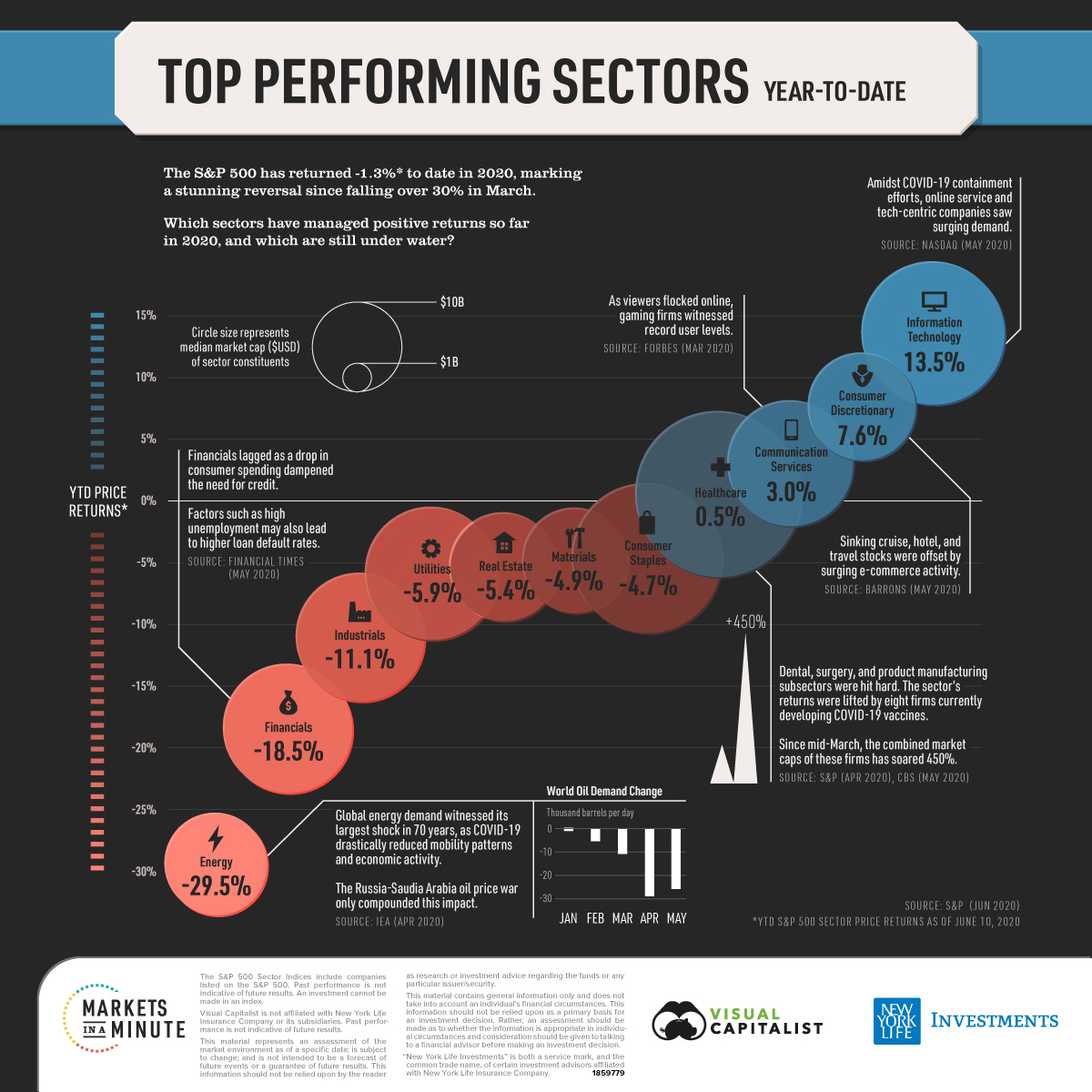

#4 Market Bubble?

Is the whole market a bubble or just specific sectors like Technology and SPACs. A new age of Covid Investors has begun, pumping printed money into the stock market.

Here you can see the break away technology has had compared to the rest of the market just up to the COVID Dip. Mostly lead by the big name companies like Amazon, Apple, Facebook, Microsoft, and Tesla. Also don’t ignore the amazing amount of technology related SPACs that have IPOed with ridiculous returns.

Another concerning trend aiding the potential bubble is the age of SPACs. SPACs are relatively old but have become a hot topic for trades in the last 6 months. Just from 2019 to 2020 the total number of SPACs that where successful and IPOed increased by 420% and the amount of capital raised increased by 612%.

This rally can not last forever and correction will happen in due time. The higher it goes the more of a chance the bubble will implode. Buying a stock because of a split is common but the disconnect between a split-induced surge and a fundamentally unchanged company means investors are paying more money for the same amount of value. That’s a sign that the game has turned psychological and euphoria over future gains, rather than improving fundamentals, which has become the primary driver of growth. The effect of the dot-com era which shows how a stock split driven market boom can end in an utter disaster has never been more prevalent to the times we are living in right now.

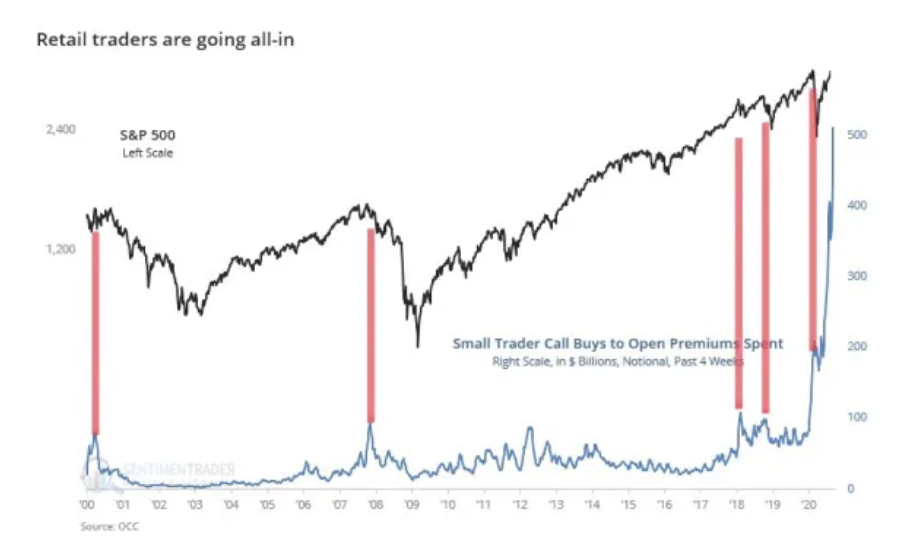

#5 Interest Rates

Interest rates are at an all time low. In fact if you have been living under a rock you would have missed the best opportunity to get a loan from the bank because interest rates are at 0%.

So, The Federal Bank leader Jerome Powell cut interest rates to 0% last March. The last time we saw this was in December of 2008, the previous recession, let that sink in. We are in a clear bubble, and in no time, the stock market is bound to burst. When interest rates are this low, it inflated stock prices as we have right now. Since 2018 each stock market correction has been more significant than the previous. Are we in a dead cat bounce like the great depression? I’m not sure, but I am sure that a correction is bound to happen, and as investors, we want to be ready.

The fed rate as 0% helps the average American with good credit; it means very low monthly interest costs for home and car buyers, businesses, and other borrowers. The Federal Banks’ decision to cut interest rates has sent interest rates on credit card offers down to their lowest levels in years. This is great for people with high credit scores, but it will make it much harder to get loans, mortgages, and credit cards for people with bad credit scores. Credit companies are even starting to lower credit limits, so people don’t take advantage of low rates.

The point is is that this cannot last forever and the Fed will be increasing the interest rates. When is that? maybe 6 months… maybe 12 months… maybe in 2 weeks, no one knows. The important thing is to be aware of this situation and use it to your current advantage at the moment and to also be prepared for when the Fed increases interest rates.

#6 Education Turmoil

The issues in the lower levels of education is what is really bothers me. I could not imagine 8 year old me being able to sit in front of a computer screen for 7 hours a day trying to learn math, science, history, and English. What’s is also really concerning is the difficultly some teachers are causing when it comes to being a teacher!! (But also their are teachers that have gone above and beyond their expectations). A family member of mine is part of the school board and has dedicated their life to educating the young and trying to improve education. To hear that some high & middle school teachers are just emailing packets of weeks worth of notes, practice problems, and assignments while giving little assistance is pathetic. The educational turmoil will recoil in the future years. In fact I hope this turmoil will show that the current education system is flawed and needs adjusting, as once said here by my partner. With young children being online at school how is this going to affect them socially? Will schools start having higher drop out rates due to classes being online? How much effect is this having in elementary schools and middle schools?

Another interesting point is the current job market for recent graduates. My partner and myself are in this boat. Currently looking for entry level positions and knowing some friends who are either having issues finding jobs or are being turned back to school for one more year to get a masters. It is obvious COVID has stirred the pot in everyone’s life. I think what everyone needs to realize is that this is what life has in store for us and what ever happens you got to keep your head held high and push through while trying to reach your goals and be the best version of yourself for your family and the people around you.

Leave a comment