A 401k is a retirement fund. The concept behind a 401k is to help young adults plan for their future. Teaching the lesson of investing early and investing a little each week. By doing this you can open yourself up to having a 401k worth over $1,000,000 after 30 years of investing and being able to leverage your account to make large purchases like a house!

Being a young adult myself I can see why people my age might overlook planning ahead and completely spend their paychecks on the weekends. It’s the first time in our lives we are getting paid and all we want to do is enjoy ourselves. This is okay but what will separate a future millionaire from your average joe is having the discipline to invest a little bit of your paycheck every week into a 401k.

Most companies you will work for will be offering a 401k retirement plan so let us do a deep dive into some of the details, benefits, and possible outcomes of investing in a 401k retirement plan.

401k Details

Your place of employment will most likely have an account with brokerages like Fidelity, TD Ameritrade, and Charles Schwab. All these brokerages offer a platform for your 401k. Within the account, you will be able to select how much of your paycheck you want to invest in a 401k.

What is most important is that a 401k pulls money from your paycheck before taxes! This is huge as you will save a couple of thousand dollars a year in taxes by moving money into your 401k. So allocating money is a tax haven and you will not be taxed until it is time to remove money from your 401k, way way down the road. At the age of 59.5 years old is when you are allowed to start pulling money out of your 401k.

Now for the year 2022, the government increased 401k allocations to a maximum of $20,500 a year. This means that every week if you decide to maximize this option, about $394 of your paycheck will be invested. (This is highly recommended). Your account will first ask you how much money you want to put towards your 401k.

Next, you will be asked to pick what funds you’d like to be invested in. In a 401k you are NOT ALLOWED to trade stocks and options. You must select from the provided list of mutual funds your brokerage is providing for your 401k.

I highly recommended googling what the funds are and seeing what stocks are held inside the fund. This type of fund is much like an ETF where the brokerage will decide what stocks comprise the fund. For example, there is a Fidelity Mid Cap Index Fund you could allocate your paycheck. Here is a breakdown of the fund’s top ten holdings.

So, what mutual funds are you choosing? There are high, medium, and low-risk mutual funds. Are you going 100% into one fund or dividing it into sections. You can opt for an 80:20 split with 80% in large-cap, low-risk mutual funds, and 20% in medium cap, medium risk mutual funds. This is entirely up to you.

Bonus – Company Matching

Does your company offer a matching program? If so, that is basically like getting a bonus every paycheck. Some companies will do a 20%, 50%, or 100% match of your contributions. IF YOUR COMPANY IS DOING A 100% MATCH PLEASE MAX OUT YOUR 401K ALLOCATIONS. If you are maxing out your 401k, putting in the government limit of $20,500, then you are technically receiving an additional $20,500 of pay a year. This will compound over time and set you up nicely for retirement. Let us look at some examples below.

Example

For example, let’s say you choose the S&P 500 Mutual Fund which has an average rate of return of 8% per year and you invest in your 401k for 30 years in a row. Using an Annuity Calculator we have come up with three scenarios.

Scenario 1 – 50% allocation

In this scenario, 50% means you are investing $10,250 a year into your S&P 500 Mutual fund with 8% growth per year. Below shows the growth of your money over 30 years.

Year 0 – $0.00

Year 1 – $11,070.00

Year 2 – $23,025.60

Year 3 – $35,937.65

Year 4 – $49,882.66

Year 5 – $64,943.27

Year 10 – $160,366.25

Year 15 – $300,573.90

Year 20 – $506,584.94

Year 30 – $1,254,045.15

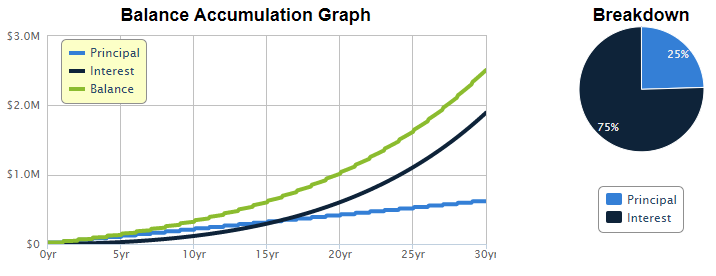

Scenario 2 – 100% Allocation (Highly Recommend)

In the following scenario, you are maxing out your 401k and allocating $20,500 of your paycheck a year into the S&P 500 Mutual Fund with 8% growth per year. Below shows your account growth over 30 years.

Year 0 – $0

Year 1 – $22,140.00

Year 2 – $46,051.20

Year 3 – $71,875.30

Year 4 – $99,765.32

Year 5 – $129,886.55

Year 10 – $320,732.49

Year 15 – $601,147.80

Year 20 – $1,013,169.89

Year 30 – $2,508,090.29

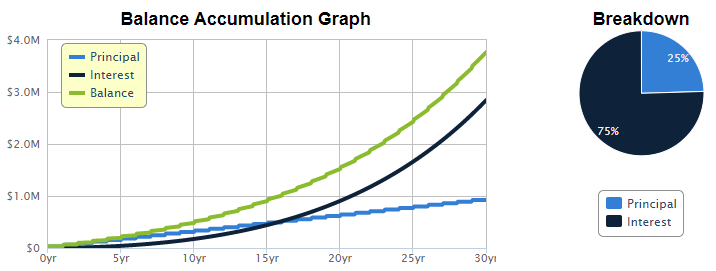

Scenario 3 – 100% Allocation w/ 50% Company Matching

In this scenario, you are investing the full $20,500 and your company is doing a 50% matchmaking of your full yearly contributions of $30,750 a year into the S&P 500 Mutual Fund with 8% growth per year. Below shows your account growth over 30 years.

Year 0 – $0

Year 1 – $33,210.00

Year 2 – $69,076.80

Year 3 – $107,812.94

Year 4 – $149,647.98

Year 5 – $194,829.82

Year 10 – $481,098.74

Year 15 – $901,721.70

Year 20 – $1,519,754.83

Year 30 – $3,762,135.44

So doesn’t a 401k sound great? Most likely you will fall somewhere in-between these three scenarios. Not every company has a matching program and you may decide to not maximize your allocations.

A 401k is great for individuals who are looking to park their money in a stable and secure investing plan. This kind of investment is very risk-averse and will provide you with great returns throughout your life.

Something young adults might not know is when you are 32 years old, recently, married, and looking to purchase a house, you will be able to leverage your 401k to receive a loan! By showing the bank your 401k they will feel more comfortable giving you loans at better rates. There are also other perks and ways to pull money out in an emergency. But these perks will not be available if you do not use the 401k to your benefit. So start reaching out to your HR team and see what kind of plans they offer!

What are 3 benefits of a 401k?

The three main benefits are tax advantages since you are investing pre-tax dollars directly from your paycheck. Time is on your side, as Warren Buffet says Ït is not about timing the market, it is about time in the market” The longer you are invested the more returns you will have in a 401k. Lastly, you can take a 401k with you when you decide to switch jobs! they are called rollovers!

Can you Lose Money in a 401k?

ABSOLUTELY! Be careful. over a short period of time, the mutual funds you invest in can have a downward trend and you could be in the red! The idea is to hold these investments for over 10 years! This was you combat the short term price fluctuations.

Do you pay Taxes on 401k?

Initially, you do not pay any taxes on a 401k when you are direct depositing money from your paychecks! But when the time comes to pull your money out you will incur taxes.

Closing Remarks

So personally we here at FinancialFreedom101 don’t believe in having a 401k. For some individuals, a 401k is a great plan, but if you follow the stock market and conduct good research before investing then a 401k is NOT FOR YOU. We do not plan to work a 9-5 job till retirement age and feel it is more beneficial for individuals like us to use an IRA as our retirement fund. An IRA provides several future tax breaks and this will be beneficial for us. Being in a 401k as an investor makes you diversified and this is something Bodhi and I are against and have explained extensively in a post called Diversification.

Check out Bodhi’s post on what types of IRAs are available. Also, check out his post on Roth IRAs to see why we have chosen this as our retirement fund.

Leave a comment