Are you tired of paying taxes on your capital gains? Want to save for retirement tax-free while controlling what you invest in, then a ROTH IRA is for you. If you are using a regular brokerage account and plan on saving for retirement that way, you are doing it all wrong; a ROTH ira is necessary.

What is a Roth IRA?

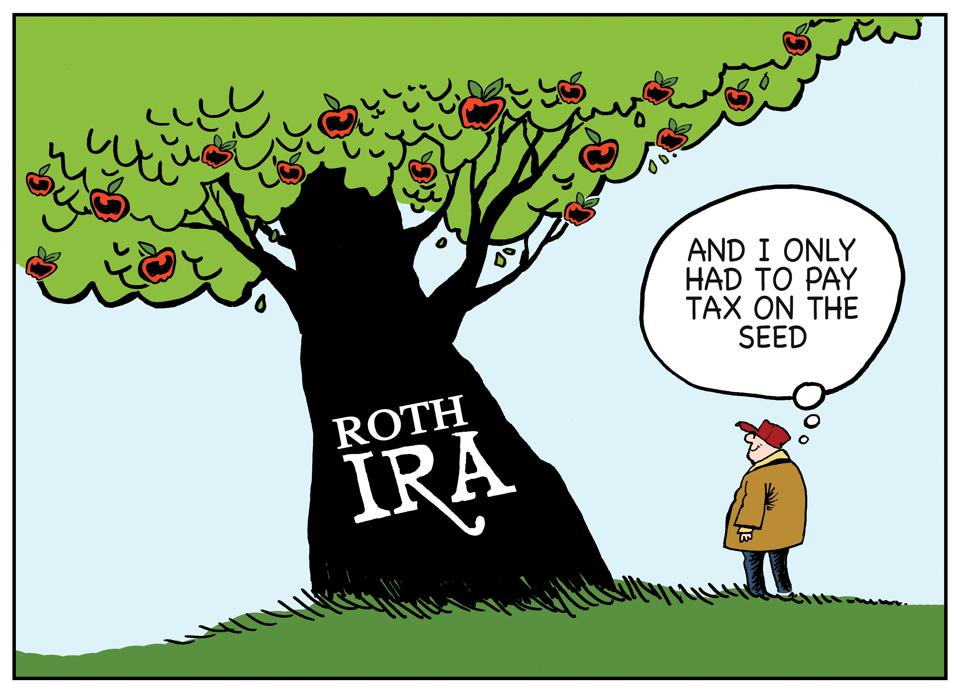

A ROTH IRA is an Individual retirement account (IRA) that allows qualified withdrawals on a tax-free basis provided certain conditions are satisfied. Established in 1997, it was named after William Roth, a former Delaware Senator. You fund a Roth with after-tax dollars, Which means you have already paid taxes on the money you put into it. In return, there is no up-front tax break; your money grows and grows tax-free, and when you withdraw after age 59½, gains are 100% tax-free and penalty-free.

Roth IRA Advantages

Tax-Free Retirement Income

Roths offer more flexibility than a Simple IRA; with a Roth, you contribute money you have already been taxed for. There is not a tax deduction as there would be with a traditional IRA. You may withdraw your contributions to a Roth IRA penalty-free at any time for any reason.

When you decide to pull your money out of your ROTH IRA, you don’t own taxes on it because you already paid taxes on the money you have contributed. But with a traditional IRA, when you pull the money out, you immediately owe income taxes. The advantage Roths have over traditional is when you take your money out, you get the full value compared to a Traditional IRA, where you get taxed upon withdrawal. The maximum annual contribution to a ROTH IRA in 2020 is $6,000.

There are multiple ways to fund a Roth ira:

- Regular contributions

- Spousal IRA contributions

- Transfers

- Rollover contributions

- 1035 exchange

Early Access to your money

You can always withdrawal Roth contributions with no penalty at any age. The 5-Year rule allows you to withdraw funds from your Roth when you wish at the rate you want to. The five-year rule applies in three situations: if you withdraw account earnings if you convert a traditional IRA to a Roth, and if a beneficiary inherits a Roth IRA. The five-year clock starts with your first contribution to any Roth IRA— There are many exceptions to taking your money out of a Roth.

Reasons to access your money tax-free

- Unreimbursed Medical Expenses.

- Health Insurance Premiums While Unemployed.

- A Permanent Disability.

- Higher-Education Expenses.

- You Inherit an IRA.

- To Buy, Build, or Rebuild a Home.

- Substantially Equal Periodic Payments.

- To Fulfill an IRS Levy.

High earners have a ‘backdoor’ entry.

A backdoor Roth IRA is a traditional way to get around the income limits that typically restrict high earners from contributing to a regular Roth Ira. a backdoor Roth IRA is a savings strategy that helps you save retirement funds in a Roth IRA even though your annual income would otherwise disqualify you from accessing this type of individual retirement account.

To open up a backdoor Roth ira, you have to open a traditional IRA and make a nondeductible contribution to it; then, you convert it into a ROTH IRA. You can also do a backdoor Roth IRA by converting deductible contributions held in a traditional IRA or a traditional 401(k) to a Roth IRA.

5 Key Characteristics of a Roth IRA

- You pay taxes on the money you put in the account. You cannot deduct the contributions on your taxes.

- In 2020 and 2021, you can contribute up to $6,000 ($7,000 if you’re 50 or older).

- You could not contribute to a Roth IRA if your modified adjusted gross income (MAGI) were more than $139,000 in 2020 (single filers) or $206,000 (married filing jointly). In 2021 the MAGI limit is $140,000 (single filers) or $208,000 (married filing jointly). (The backdoor strategy offers a workaround to these limits.)

- People at least 59½ years old and hold their accounts for at least five years can take distributions, including earnings, without paying federal taxes.

- You don’t have to take any money out of your Roth IRA if you don’t want to. There are no required minimum distributions (RMDs).

Sample Roth IRA Portfolio

Contribution- $6,000 a year

Investing in dividend aristocrats:

Altria- 50 shares

Chevron- 20 shares

National Health Investors- 30 Shares

IF you planned on holding this portfolio for 40 years, the total physical dollar amount you put in would be $240,000. The portfolio would guarantee you an average of 7% dividend yield over the entire portfolio each year reinvested; with the average annual growth rate of 10% over 40 years, you would come out with $4,066,396.89 tax-free. You will make $3,826,396.89 over 40 years if you stick to your investment plan.

How to Open up a Roth IRA

You can open up a Roth IRA at a brokerage or a bank. You choose your self how you want the money invested like a typical broker account. You can choose what you want to invest your money in, such as mutual funds, stocks, bonds, exchange-traded funds (ETFs), or bank savings products. You can add money in over a time by a lump sum each year, or you can dollar cost average up to $6000 a year. If you’re looking to open up a ROTH, I suggest you open it with your broker or bank in an app or site with an interface you use to. Opening up a Roth will be super beneficial for you and your financial future.

Leave a comment